Payday Super — What We Know today

Payday Super is now law — here's what every employer needs to know before 1 July 2026

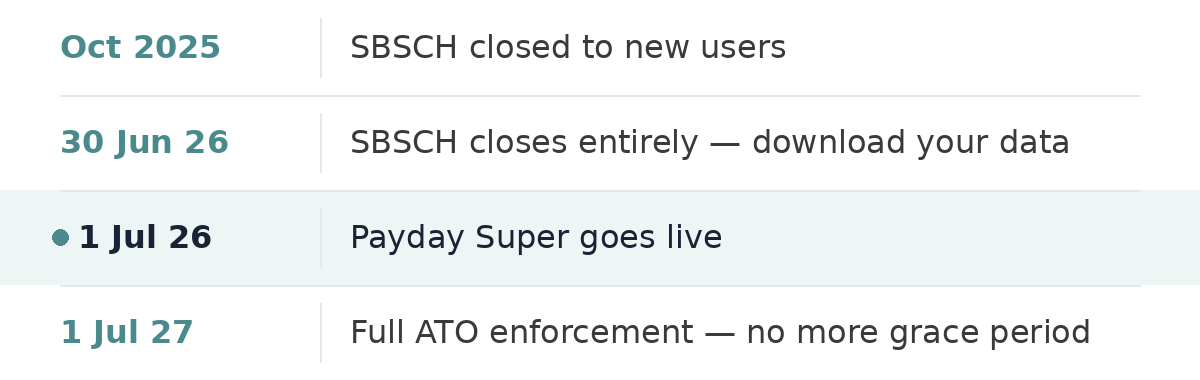

Key Dates

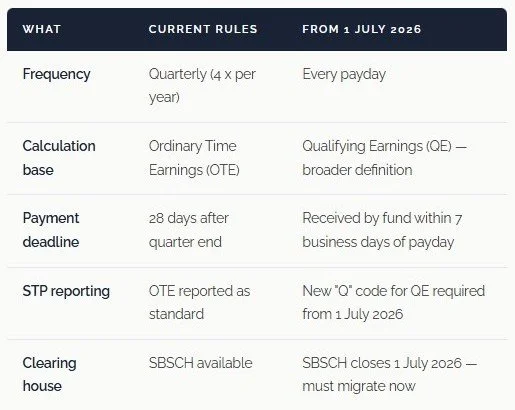

What's Actually Changing?

ATO Resources

Bookmark the ATO's Payday Super page for the latest updates, fact sheets and checklists.

A note from Wendy

This is the most significant change to employer superannuation since compulsory super was introduced — and with just months until the start date, preparation really can't wait. The good news is that if you're already using Xero and paying super regularly, you're in a strong position. It's mainly about updating your processes, your STP reporting, and your clearing house arrangement.

If you're not sure where your business stands, the best thing you can do is have a conversation now — before 1 July arrives and the pressure is on.

Not sure if your payroll is ready?

We offer a free 1-hour consultation — no obligation, no sales pitch. Let's talk through your payroll setup and make sure you're ready for Payday Super before 1 July 2026.

wendy@bookbalance.com.au | 0400 131 072

If you pay employees, this affects you. From 1 July 2026, superannuation guarantee must be paid on every single payday — not quarterly. The legislation has passed Parliament and there are just months left to get ready. Here's a plain-English breakdown of everything we know right now.

What is Payday Super?

Payday Super is a major change to how and when employers pay superannuation guarantee (SG) contributions. Right now, you're required to pay SG at least once per quarter — with contributions due 28 days after the end of each quarter.

From 1 July 2026, that changes entirely. SG must be paid on every payday, and those contributions must be received by the employee's super fund within 7 business days of each payday.

The Treasury Laws Amendment (Payday Superannuation) Act 2025 and the Superannuation Guarantee Charge Amendment Act 2025 have both passed Parliament — this is now law, not a proposal.

What are Qualifying Earnings (QE)?

This is one of the most important changes to understand. Super is currently calculated on Ordinary Time Earnings (OTE). Under Payday Super, it will be calculated on Qualifying Earnings (QE) — a broader definition that includes:

Ordinary time earnings (OTE) — as before

Salary sacrifice contributions — now included in the base

Other amounts currently included in salary or wages for SG

This matters because for some employees, the SG liability will be higher under QE than under OTE. It's worth reviewing your payroll calculations before the changeover date.

What about the Super Guarantee Charge?

If contributions aren't received by the super fund within 7 business days of payday, the Super Guarantee Charge (SGC) applies. The new SGC is significantly more punishing than before:

Calculated on QE (not OTE) — wider base

Not tax deductible — unlike voluntary late payments

Includes an administrative uplift based on compliance history

Maximum penalty of 200% of SGC

Repeat offenders face penalties of 25–50% of unpaid SGC

SBSCH is closing — act now

The ATO's Small Business Superannuation Clearing House (SBSCH) is being retired. It closed to new users on 1 October 2025, and closes entirely on 30 June 2026. If you currently use SBSCH, you must:

Find an alternative clearing house or payroll solution now

Download your historical SBSCH data before 30 June 2026

Ensure your new solution supports the increased frequency of Payday Super payments

Many payroll software providers — including Xero — already offer integrated super payment solutions that will support Payday Super from day one.

Your Payday Super checklist

Review your payroll cycle — align super payment runs to your pay cycle and confirm your software can handle more frequent payments.

Understand QE — check which earnings components fall under Qualifying Earnings. The base is broader than OTE.

Update STP reporting — confirm your payroll software will support the new "Q" earnings code from 1 July 2026.

Migrate off SBSCH — find an alternative and transition before 30 June 2026. Download your history first.

Check employee fund details — resolve outstanding fund errors before the deadline to avoid failing the 7-day rule.

Review your cash flow — more frequent super payments may affect working capital. Plan ahead.

Closely held employees — directors paid via fees are covered by Payday Super. Sole traders and partners receiving distributions are not.

The ATO's first-year approach

The ATO has released Practical Compliance Guideline PCG 2026/1, which outlines a risk-based approach for the period 1 July 2026 to 30 June 2027. Employers are classified into three risk zones:

Low Risk

Who: Employers who attempt to pay SG on time and correct errors as soon as reasonably practicable. ATO approach: Not the focus of compliance action during Year 1. Full enforcement kicks in from 1 July 2027.

Medium Risk

Who: Employers with some delays or partial corrections. ATO approach: May receive ATO guidance and must demonstrate improvement during the transition year.

High Risk

Who: Employers with individual final SG shortfalls greater than nil after 28 days following the end of the quarter. ATO approach: Subject to compliance action even during Year 1. No grace period applies.

⚠️ The first-year grace period applies only to QE days from 1 July 2026 to 30 June 2027.

From 1 July 2027, full enforcement applies to all employers, regardless of risk zone.