Bookkeeping for Sole Traders: A Complete Starter Guide

What records to keep, how to track your income and expenses, what you can and can't claim — and when it's time to ask for help.

Whether you're a tradie, freelancer, consultant, or running a small online business, good bookkeeping is one of the most practical things you can do for your business. Not just for tax time — for your peace of mind every single day.

I see a lot of sole traders who've been winging it for a year or two before they reach out. By then there's usually a backlog of unreconciled transactions, vague memories of cash expenses, and a mild dread whenever the ATO comes to mind. It doesn't have to be that way.

Here's everything you need to know to get set up right from the start — or to finally get on top of things if you've been putting it off.

What records do you need to keep?

The ATO requires you to keep business records for at least five years. The clock generally starts from when you prepared or obtained the record, or completed the transaction — whichever is later. For most day-to-day records that means five years from the date of the transaction, not from when you lodge your return. That sounds like a long time — but with the right system, it's genuinely painless.

Expense records

Receipts and invoices for all business purchases

Bank and credit card statements

Loan and lease agreements

Vehicle logbooks if you're claiming motor vehicle expenses

Stock purchase and sales records (if applicable)

Income records

Invoices you issue to clients and customers

Bank statements showing payments received

Sales receipts (including EFTPOS records)

Records of any other income — grants, asset sales, interest

Other essentials

Your ABN registration details

GST records if your annual turnover is $75,000 or more

Superannuation records if you engage contractors who are entitled to super

PAYG payment summaries if you pay wages

How to track your income and expenses

This is where a lot of sole traders come unstuck — not because they're disorganised people, but because nobody ever told them what a simple, sustainable system actually looks like.

Step one: Separate your finances

Open a dedicated business bank account and use it only for business income and expenses. This single step makes everything else easier — reconciliation, BAS, tax return, the lot. If your personal and business transactions are mixed together, untangling them takes time and costs money.

Step two: Choose a tracking method that suits your business

For very simple businesses with just a handful of transactions a month, a spreadsheet can work. But for most sole traders — especially anyone registered for GST — cloud accounting software is genuinely worth the monthly subscription. It connects directly to your bank, codes transactions automatically, and produces the GST figures your BAS needs without you having to calculate anything manually.

The main options for Australian businesses are Xero, MYOB, and QuickBooks. I'm a Xero Certified Advisor, so it's what I know best and what I recommend to most of my clients — but the right choice depends on your industry and how you work.

Step three: Build a simple weekly habit

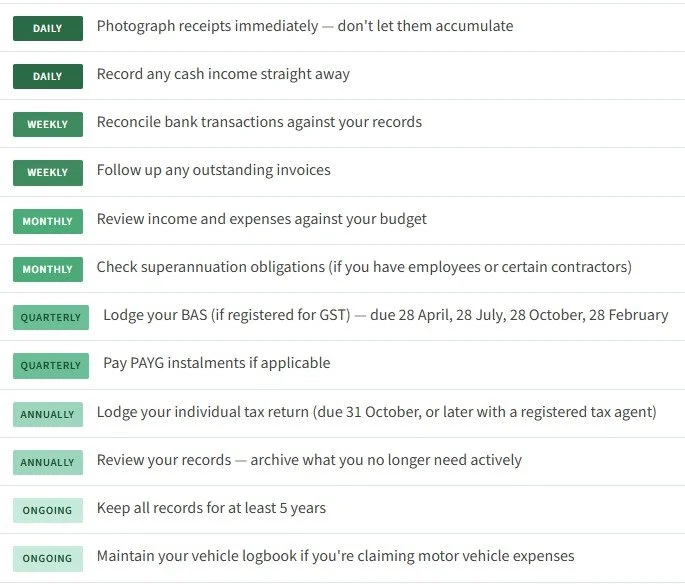

Photograph receipts the moment you get them — don't let them pile up

Reconcile your bank transactions once a week while they're fresh

Invoice promptly and follow up anything overdue within 7 days

Do a quick monthly review of income versus expenses

What can you claim — and what can't you?

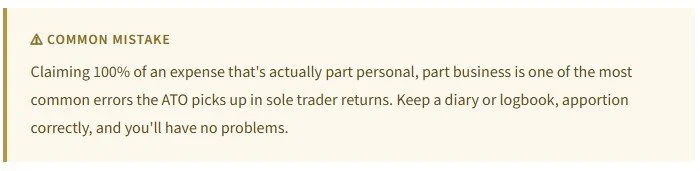

The golden rule: you can claim deductions for expenses that are directly related to earning your business income. You must have a record, and if an expense has personal use mixed in, you can only claim the business portion.

GST — do you need to register?

If your turnover reaches $75,000 in any 12-month period (current or projected), you must register for GST. Once registered, you add 10% to your invoices, claim back GST on eligible business purchases, and lodge a Business Activity Statement (BAS) — usually quarterly.

If you're under the threshold, registration is optional. Some businesses register anyway to claim input tax credits on their expenses. Whether that makes sense depends on your margins and your customers — it's worth a conversation if you're not sure.

When should you get professional help?

DIY bookkeeping can work well — especially at the start, when your business is simple and your transaction volume is low. But there are certain moments when getting a professional involved pays for itself many times over.

Consider getting help if:

You're approaching or have crossed the $75,000 GST threshold

You've taken on your first employee or subcontractor

You're behind on your BAS or tax returns

You're spending more than 2–3 hours a week on bookkeeping

You're genuinely unsure what you can and can't claim

You've received any correspondence from the ATO

You're applying for a business loan or home mortgage

You want to understand your numbers so you can actually grow

A registered BAS agent is legally authorised to prepare and lodge your BAS on your behalf — something an unregistered bookkeeper can't do. You can verify credentials on the Tax Practitioners Board register at tpb.gov.au.

Quick reference: your sole trader bookkeeping checklist

The sooner you get a clean system in place, the easier everything else becomes — BAS, tax, loan applications, and knowing whether your business is actually making money.

If you'd like help setting things up or getting on top of a backlog, I'd love to chat.